Adobe's Persistent Post-Earnings Sell-Offs: Identifying the Common Themes

We asked Gemini 2.5 Flash for some Deep Research notes

This post was originally linked in the lede of Friday’s note. Everything below was written by Gemini. The only two things I did were ask the following question and format the included table to work on Substack. I figured folks might find it interesting to get a sense of what can be done.

Friday was the seventh out of the last eight earnings reports where Adobe sold off more that four percent on day. Is there a common theme?

I. Executive Summary

Adobe (ADBE) has demonstrated a notable and consistent pattern of significant stock depreciation following its quarterly earnings announcements. In seven of the last eight reporting periods, the company's stock has sold off by more than four percent on the day of the release. This recurring negative market reaction persists despite Adobe frequently reporting financial results that meet or even exceed analyst expectations for the current quarter.

The underlying factors driving this persistent investor skepticism are multifaceted, primarily stemming from a perceived disconnect between Adobe's actual financial performance and Wall Street's elevated forward-looking growth expectations. The predominant themes contributing to these sell-offs include:

Conservative or "Light" Forward Guidance: Adobe's outlook for upcoming quarters frequently falls short of aggressive analyst consensus, triggering immediate negative sentiment.

Uncertainty Regarding AI Monetization Pace: Despite substantial investments and widespread adoption of its artificial intelligence (AI) innovations, particularly Firefly, investors remain unconvinced about the speed and magnitude of these initiatives translating into accelerated and tangible financial returns.

Heightened Competitive Pressures: The emergence of new competitors and alternative solutions, especially in the generative AI space, fuels concerns about Adobe's long-term market share and pricing power.

Perceived Growth Deceleration: The market's re-evaluation of Adobe's growth trajectory, shifting from a high-growth stock to a more mature entity, often leads to a lower valuation multiple if growth is not demonstrably accelerating.

II. Introduction: The Adobe Earnings Paradox

The observation that Adobe's stock consistently experiences sharp declines after its earnings reports, even when the company announces strong financial performance, presents a compelling paradox for market participants. The user's query specifically highlights this peculiar and financially significant trend: "Friday was the seventh out of the last eight earnings reports where Adobe sold off more that four percent on day. Is there a common theme?" This phenomenon challenges the conventional market wisdom that positive financial results should lead to a favorable stock reaction.

This report undertakes a comprehensive analysis of Adobe's recent earnings cycles, meticulously examining the last eight fiscal quarters. The objective is to dissect the reported financial results, analyze the immediate market reactions, and synthesize the various stated and implied reasons behind these recurring sell-offs. By delving into the granular details of each reporting period, this analysis aims to uncover the common threads that explain this seemingly counterintuitive behavior and provide a deeper understanding of the investor sentiment surrounding ADBE.

III. Quarterly Performance and Market Reactions: A Detailed Review

To systematically identify the common themes, a detailed review of Adobe's financial performance for each of the last eight fiscal quarters is essential. This section outlines the reported revenue and earnings per share (EPS) against analyst expectations, critically analyzes the immediate market reaction, and synthesizes the attributed reasons for the stock movement, drawing directly from financial news and company statements. This granular examination is crucial for pinpointing recurring patterns and underlying causes.

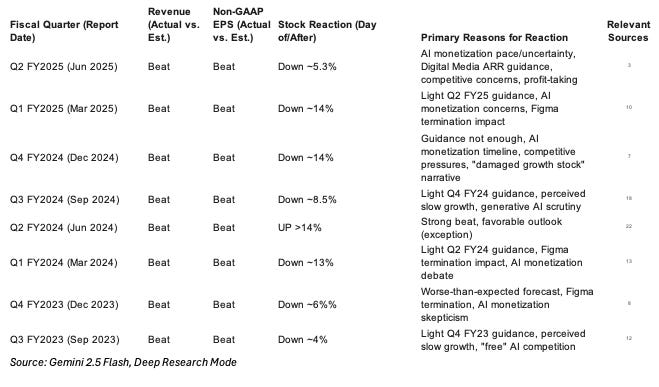

Adobe Quarterly Earnings Summary: Performance, Stock Reaction, and Key Drivers (Last 8 Quarters)

Detailed Quarterly Analysis

Q2 FY2025 (Reported June 2025): Adobe reported record revenue of $5.87 billion and non-GAAP EPS of $5.06, both surpassing analyst expectations of $5.8 billion revenue and $4.97 EPS, respectively. The Digital Media and Digital Experience segments exhibited robust year-over-year growth of 11% and 10%, respectively. Furthermore, the company raised its full-year outlook for both revenue and EPS.1 Despite these objectively strong results, the stock declined by approximately 5.3% on the day.4

The primary factors contributing to this decline were investor skepticism regarding the pace of monetizing AI initiatives and a slower-than-anticipated acceleration in AI-driven growth.1 Analysts noted that while management expressed positivity about demand, it would require more time to demonstrate the full financial impact of AI initiatives.8 Although the full-year revenue guidance was raised, the outlook for the Digital Media segment's Annual Recurring Revenue (ARR) growth was maintained at 11%. Some analysts interpreted this as implying a deceleration in the second half of the fiscal year, which dampened enthusiasm.7 Ongoing competitive pressures were also cited as a contributing factor.7 Additionally, some market observers attributed a portion of the sell-off to profit-taking after a recent stock rebound.5

This quarter highlighted a critical market dynamic: the "Show Me the Money" AI dilemma. Despite Adobe's clear innovation and significant user engagement with AI, as evidenced by 24 billion generations across Firefly and Creative Cloud and Firefly app paid subscriptions nearly doubling sequentially 4, the market remains unconvinced about the

rate at which this usage translates into substantial, accelerating financial growth. This suggests a disconnect in the investment thesis, where investors demand to see AI not merely as a defensive feature or incremental improvement, but as a direct, significant driver of accelerated revenue and ARR growth that goes beyond current guidance and justifies a higher valuation multiple. The concern is not if AI will benefit Adobe, but when and how much it will meaningfully impact the top-line growth trajectory.

Furthermore, this period underscored that guidance acts as the primary market driver. Even with a "beat-and-raise" quarter, the market's immediate focus pivots to future guidance. If any aspect of this guidance, particularly a key metric like Digital Media ARR growth, implies deceleration or simply maintenance of current growth rates, it can trigger a negative reaction. This emphasizes the market's extreme forward-looking nature and its sensitivity to growth narratives. For a company like Adobe, which has historically commanded a growth premium, even a slight hint of future deceleration, or a lack of acceleration, can overshadow current strong performance, as the market is pricing in future growth, and any perceived softness in that outlook leads to an immediate repricing of the stock.

Q1 FY2025 (Reported March 2025): Adobe delivered record Q1 revenue of $5.71 billion, representing 10% year-over-year growth (11% in constant currency), and non-GAAP EPS of $5.08. These figures exceeded analyst expectations of $5.66 billion revenue and $4.97 EPS. Digital Media ARR grew 12.6% year-over-year, and the company reaffirmed its FY2025 targets.9 However, the stock fell 4.35% in after-hours trading 10, with some reports indicating a larger drop of nearly 14% on the day after the announcement.12

The primary reason for this sell-off was the "light" revenue guidance provided for Q2 FY2025, which ranged from $5.77 billion to $5.82 billion, falling below the analyst consensus of $5.87 billion. This signaled potentially weaker near-term demand.9 Persistent investor concerns about the monetization strategies for AI and the lingering impact of the Figma deal termination fee also contributed to the negative sentiment.10

This quarter reinforces the pattern observed in Q2 FY2025, where a "guidance miss" serves as a recurring trigger. Even with a strong beat on current quarter numbers and reaffirming full-year targets, a next-quarter guidance that falls short of aggressive analyst consensus can trigger a significant sell-off. This suggests that the market's immediate reaction is heavily weighted towards the short-term outlook, and full-year reaffirmations are often insufficient to offset a weak near-term guide.

The repeated mention of AI monetization concerns across multiple quarters 10, even when AI adoption metrics are positive (e.g., Firefly video model launched, AI book of business over $125 million ARR 10), indicates a deep-seated apprehension among investors. This suggests that the market views Adobe's current AI monetization as insufficient or too slow, questioning whether AI will truly be a significant

accelerator rather than just a cost of doing business or a defensive measure against competitors. The market is looking for a clear, exponential return on AI investment, which has not yet materialized in the financial outlook to their satisfaction.

Q4 FY2024 (Reported December 2024): Adobe reported record Q4 revenue of $5.61 billion and non-GAAP EPS of $4.81, contributing to a record $21.51 billion in full-year FY2024 revenue. The company emphasized strong demand fueled by AI innovations across its various cloud offerings.14 Despite these accomplishments, the stock declined again, with reported drops ranging between 5.3% 7 and over 13%.12 Analysts observed that even a raised revenue outlook was insufficient to satisfy Wall Street, as the maintained 11% Digital Media ARR growth outlook implied a deceleration.7 Concerns regarding competitive pressures and the extended timeline for AI to yield substantial profits continued to weigh on investor sentiment.7

The recurring sell-offs, despite strong underlying financials, suggest that the market is re-evaluating Adobe's growth profile. It appears to be struggling with the transition pain from maintaining its premium "growth stock" multiple, even as it delivers consistent, albeit not accelerating, growth. Analyst commentary explicitly refers to Adobe as a "damaged former growth stock" or questions its ability to "re-rate".7 This indicates that the market's perception of Adobe's growth potential has shifted. Investors are no longer willing to pay a high growth multiple for consistent, but not

accelerating, growth, especially when AI, a potential accelerant, is not yet fully "showing up" in the financials in a dramatic way. This repricing reflects a reclassification of the stock from a high-growth category to a more mature, value-oriented one, which often involves a downward adjustment in valuation.

Furthermore, this quarter highlights a "conservative guidance" cycle. Adobe's management often provides guidance that "could prove conservative".7 While this strategy might allow them to "beat its forecasts each quarter" 18, it consistently disappoints Wall Street's higher expectations, leading to immediate post-earnings sell-offs. This creates a recurring dynamic where Adobe sets a bar it can clear, but that bar is consistently below what the market

hopes for, particularly in terms of growth acceleration. This results in a predictable negative reaction, even if the company ultimately outperforms its own lowballed guidance.

Q3 FY2024 (Reported September 2024): Adobe exceeded expectations with $5.41 billion in revenue and $3.81 EPS (compared to a $3.63 consensus), driven by robust growth across Creative Cloud, Document Cloud, and Experience Cloud. The company emphasized strong AI integration and operational efficiency.19 However, the stock dropped approximately 10% after the earnings announcement.18 The primary driver for this decline was the Q4 FY2024 guidance, which came in below analysts' expectations ($5.50 billion-$5.55 billion revenue versus a $5.61 billion consensus), implying a growth rate (8.9%-9.9% year-over-year) that was perceived as "a touch slow" for some investors.18 Scrutiny over generative AI monetization, especially in the face of free alternatives, also contributed to the negative reaction.18

This quarter demonstrates that the market has a clear implicit threshold for what constitutes "acceptable" growth for Adobe. Even if 8.9-9.9% year-over-year growth is solid for a mature company, it is deemed "slow" by investors looking for higher returns, especially given the AI narrative. This indicates that the market is not just looking for growth, but a specific rate of growth that aligns with its high valuation expectations for a technology leader. Anything below that implicit threshold, even if it is still double-digit growth, triggers a negative reaction, suggesting that the market is demanding accelerated growth to justify its valuation, particularly when new technologies like AI are at play.

Q2 FY2024 (Reported June 2024): In stark contrast to the prevailing trend, Adobe posted better-than-expected results for Q2 FY2024, leading to a significant positive stock reaction, with shares climbing over 14% the day after the announcement.22 While specific reasons for this positive anomaly are not detailed in the provided information, its occurrence implies a combination of a strong beat on current numbers and a more favorable or unexpectedly strong forward outlook compared to other quarters. This quarter stands as the single exception to the user's observed pattern.

This "outlier" quarter and its implications are crucial. The positive reaction in Q2 FY2024 22 serves as an important counterpoint to the overall trend of post-earnings sell-offs. It indicates that if Adobe

does significantly exceed expectations and provides a sufficiently strong outlook, the stock can react positively. This suggests that the recurring sell-offs are not due to inherent flaws in Adobe's business model or its inability to deliver, but rather a consistent mismatch between investor expectations for future growth (especially AI-driven acceleration) and Adobe's communicated outlook. It highlights that the market is willing to reward Adobe, but the bar for doing so is exceptionally high.

Q1 FY2024 (Reported March 2024): Adobe reported record Q1 revenue of $5.18 billion and non-GAAP EPS of $4.48, both exceeding expectations. The company also announced a new $25 billion share repurchase program.13 Despite these positive developments, the stock declined in the days following the announcement.7 The "light" Q2 FY2024 revenue guidance ($5.25 billion-$5.30 billion), which was below analyst expectations for year-over-year growth (10.2% YoY expected vs. 8.9%-10% guided), was a primary factor.13 The $1 billion termination fee from the Figma deal also impacted GAAP EPS and created a negative overhang.13 Ongoing uncertainty about AI monetization and competitive pressures were also cited.13

This quarter further solidifies the pattern of guidance misses as a primary driver of sell-offs. The consistent nature of the "light guidance" 13 suggests it is either a deliberate conservative strategy by management or a consistent overestimation by analysts, leading to a predictable negative market reaction. This implies a fundamental mismatch between how Adobe communicates its future and how the market models it, almost guaranteeing a negative reaction if guidance is not a significant beat. This pattern suggests that analysts are consistently more optimistic about Adobe's near-term growth potential than the company itself.

Q4 FY2023 (Reported December 2023): Adobe achieved record Q4 revenue of $5.05 billion and non-GAAP EPS of $4.27, exceeding consensus estimates. The company highlighted strong Digital Media ARR and significant AI advancements, including 4.5 billion generations with Firefly.24 However, the stock tumbled more than 13%.12 The sell-off was primarily attributed to a "worse-than-expected forecast" for the upcoming quarter 12, ongoing investor skepticism regarding the timeline for AI integration to yield substantial profits 8, and the impact of the $1 billion Figma deal termination fee on GAAP EPS.13

This period illustrates how one-off events can exacerbate underlying concerns. While the Figma termination fee was a specific, non-recurring event 13 and a significant one-time charge, its occurrence amidst existing concerns about AI monetization and guidance likely amplified pre-existing investor anxieties, leading to a more severe sell-off. This suggests that while not the sole cause, such events can compound negative sentiment.

Q3 FY2023 (Reported September 2023): Adobe again set a record with $4.89 billion in revenue, up 10% year-over-year (13% in constant currency), and non-GAAP EPS of $4.09, both surpassing analyst estimates.5 The company emphasized strong subscription growth across Creative Cloud, Document Cloud, and Experience Cloud, and highlighted the integration of Firefly into Photoshop and Illustrator, with over 3 million beta users.29 Despite these positive results, the stock dropped approximately 10% to 13% after the announcement.12 The primary reason cited was the Q4 FY2023 guidance, which was below analyst expectations for both revenue ($4.975 billion-$5.025 billion vs. $5.0 billion consensus) and non-GAAP EPS ($4.10-$4.15 vs. $4.06 consensus for EPS, though some sources indicate EPS guidance was above estimates).27 Concerns about competition from "free" generative AI models like DALL-E and Canva also contributed to the negative market reaction.18

This quarter further highlights the "growth rate" threshold that the market implicitly holds for Adobe. Even if 10% year-over-year growth is solid for a mature company, it can be deemed "slow" by investors looking for higher returns, especially given the AI narrative. This indicates that the market is not just looking for growth, but a specific rate of growth that aligns with its high valuation expectations for a technology leader. Anything below that implicit threshold, even if it is still double-digit growth, can trigger a negative reaction, suggesting that the market is demanding accelerated growth to justify its valuation, particularly when new technologies like AI are at play.

IV. Unpacking the Common Themes Behind the Sell-Offs

The detailed quarterly analysis reveals several consistent themes that collectively explain Adobe's recurring post-earnings stock declines.

A. The Guidance Gap: High Expectations vs. Conservative Outlook

A pervasive theme across multiple quarters is the disconnect between Wall Street's aggressive growth expectations and Adobe's more conservative forward guidance. Time and again, even when Adobe reports a "beat" on current quarter revenue and earnings, its outlook for the next quarter or the full fiscal year often falls short of analyst consensus. For instance, in Q1 FY2025, despite strong current results, the "light" Q2 FY2025 revenue guidance signaled potentially weaker near-term demand, leading to a significant stock drop.9 Similarly, in Q3 FY2024, the Q4 guidance was perceived as "a touch slow" by investors, despite solid current performance.18

This pattern suggests that the market is inherently forward-looking and highly sensitive to growth projections. For a company like Adobe, which has historically commanded a premium valuation based on its growth trajectory, any hint of deceleration or a lack of acceleration in its future outlook can overshadow current strong performance. While Adobe's management might strategically provide guidance that "could prove conservative" to enable consistent beats on its own forecasts 7, this approach consistently frustrates growth-hungry investors who are seeking a clearer path to higher returns and expect a more ambitious outlook. The market's models are often more optimistic than the company's own projections, leading to a predictable negative reaction when those higher expectations are not met.

B. AI Monetization: The Pace of Profitability

Adobe has heavily invested in and integrated AI across its product portfolio, notably with Firefly, its generative AI model. The company frequently highlights impressive adoption metrics, such as 24 billion generations across Firefly and Creative Cloud by Q2 FY2025, and Firefly app paid subscriptions nearly doubling sequentially.4 Management expresses strong optimism about AI's role in driving future growth and profitability, with an "AI book of business" tracking above $250 million target for AI Direct ARR by the end of FY2025.4

However, a recurring concern among investors is the pace at which these AI initiatives are translating into accelerated and tangible financial returns. Analysts consistently point to "investor concerns regarding the company's pace in monetizing its artificial intelligence (AI) initiatives".1 The market is demanding to see AI not just as a defensive feature or an incremental improvement, but as a direct, substantial driver of

accelerated revenue and ARR growth that goes beyond what current guidance implies. The apprehension is not about the potential of AI for Adobe, but about the timeline and magnitude of its financial impact. This "show me the money" sentiment from the market indicates that adoption and innovation alone are insufficient; investors require clear evidence of how AI will significantly boost the top-line growth trajectory and justify a higher valuation multiple.

C. Competitive Pressures and Market Share Dynamics

The landscape for creative software is evolving rapidly, with the emergence of new competitors and alternative solutions, particularly in the generative AI space. Companies like Canva and DALL-E are frequently mentioned as challengers.18 The concern is that these new entrants, especially those offering "free" or lower-cost generative AI tools, could erode Adobe's market share or pressure its historically high margins.14

This competitive dynamic influences investor confidence in Adobe's long-term competitive moat and pricing power. While Adobe emphasizes its "commercially safe" Firefly models and integration across its professional-grade tools 11, the market remains vigilant about the potential for disruption. The debate over whether AI will be a benefit or a curse to Adobe's financials is a significant factor pressuring the stock.7 Investors question if Adobe can maintain its leadership and profitability in a rapidly changing environment where content creation tools are becoming more accessible and, in some cases, free.

D. Growth Trajectory: Deceleration vs. Acceleration Demands

Adobe consistently reports strong financial results, including double-digit revenue growth and record figures across its segments. For instance, FY2024 saw record revenue of $21.51 billion, an 11% year-over-year increase.14 However, despite this consistent performance, the stock often declines. This suggests that the market is re-evaluating Adobe's growth profile, perceiving a shift from a high-growth stock to a more mature entity.

Analyst commentary sometimes refers to Adobe as a "damaged former growth stock" 7, or questions its ability to "re-rate" its multiple. This indicates that investors are no longer willing to pay a high growth multiple for consistent, but not

accelerating, growth. The market has an implicit "growth rate" threshold; even if 8.9%-9.9% year-over-year growth is solid for a mature company, it is deemed "slow" by investors seeking higher returns, especially given the AI narrative.18 This repricing reflects a reclassification of the stock, often involving a downward adjustment in valuation, as investors demand evidence of accelerated growth to justify a premium.

E. Broader Market Sentiment and Profit-Taking

While the primary drivers are company-specific, broader market sentiment and investor behavior can also play a role. For example, after Q2 FY2025 earnings, some analysts attributed part of the stock's decline to profit-taking following a recent 25% rebound from April lows.5 This suggests that even when results are positive, if the stock has run up significantly prior to the announcement, some investors may choose to lock in gains, contributing to a post-earnings sell-off. Furthermore, general macroeconomic conditions and geopolitical tensions can also influence investor caution.1

V. Conclusion: Navigating Investor Sentiment and Future Outlook

The recurring post-earnings sell-offs of Adobe's stock, observed in seven of the last eight quarters, are not indicative of a company in financial distress. On the contrary, Adobe consistently delivers strong financial performance, often exceeding current quarter revenue and earnings expectations. The core issue lies in a persistent and significant misalignment between Adobe's conservative forward-looking guidance and Wall Street's exceptionally high expectations for accelerated growth, particularly driven by AI monetization.

The market's skepticism regarding the pace and magnitude of AI's financial impact, coupled with concerns about competitive pressures from emerging, often free, alternatives, creates a challenging narrative for Adobe. Investors are demanding clear, quantifiable evidence of how AI will translate into substantial, accelerated revenue and ARR growth, beyond the consistent double-digit growth rates already being achieved. The stock's reaction suggests a re-evaluation of Adobe's growth profile, moving from a premium "growth stock" to a more mature, "value-oriented" one, which inherently commands a lower valuation multiple if dramatic acceleration is not evident.

The single exception to this pattern, Q2 FY2024, where the stock surged over 14% 22, highlights that the market

is willing to reward Adobe, but the bar for doing so is exceptionally high. It requires not just a beat on current numbers, but a forward outlook that genuinely surprises to the upside and convincingly addresses the market's demands for AI-driven acceleration and competitive resilience.

VI. Recommendations for Investors

For investors considering Adobe stock, a nuanced perspective is crucial. The company's underlying business fundamentals remain strong, characterized by high gross profit margins (89%), robust operating profit margins (36%), and a scalable subscription model.14 Its continued innovation in AI, particularly with Firefly, is driving user engagement and has the potential to influence billions in ARR.10

However, investors should monitor the following key metrics and narratives:

AI Monetization Clarity: Look for more explicit details and accelerated growth figures directly attributable to AI initiatives in future earnings reports. The market needs to see the "AI book of business" translate into a tangible acceleration of overall revenue and ARR growth, rather than just adoption metrics.

Guidance vs. Expectations: Pay close attention to Adobe's forward guidance, particularly for Digital Media ARR growth. Understand that even "conservative" guidance, while potentially leading to internal beats, may continue to disappoint Wall Street's higher expectations and trigger short-term sell-offs.

Competitive Landscape: Evaluate how Adobe's new offerings and pricing strategies (e.g., upcoming price increases 7) are effectively countering competitive pressures from free or lower-cost alternatives. Assess whether Adobe can maintain its market share and pricing power in the evolving creative software market.

Long-Term Growth Trajectory: Reconcile Adobe's consistent double-digit growth with the market's demand for acceleration. Investors with a long-term horizon may find value in Adobe's stable, profitable business at current valuations (e.g., 20x expected adjusted earnings vs. a 3-year average of 25x 1), but those seeking rapid growth may remain on the sidelines until a clear acceleration narrative emerges.

In conclusion, Adobe's stock performance post-earnings is less about fundamental weakness and more about a persistent mismatch between its steady, robust growth and the market's insatiable appetite for accelerated returns, particularly from its AI investments. Understanding these underlying themes is key to navigating the stock's volatility and making informed investment decisions.

Works cited

How Did Adobe Fare In Q2? - Trefis, accessed June 14, 2025, https://www.trefis.com/stock/adbe/articles/566680/how-did-adobe-fare-in-q2/2025-06-13

ADBE Q2FY25 Earnings Press Release - Adobe, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/12605202/a654erthgf.pdf

Adobe Q2 Earnings Beat Estimates, Revenue Up Y/Y, Shares Fall | Nasdaq, accessed June 14, 2025, https://www.nasdaq.com/articles/adobe-q2-earnings-beat-estimates-revenue-y-y-shares-fall

Adobe ADBE Q2 2025 Earnings Call Transcript | The Motley Fool, accessed June 14, 2025, https://www.fool.com/earnings/call-transcripts/2025/06/13/adobe-adbe-q2-2025-earnings-call-transcript/

Adobe Reports AI-Fueled Earnings Beat - Nasdaq, accessed June 14, 2025, https://www.nasdaq.com/articles/adobe-reports-ai-fueled-earnings-beat

Adobe Posts Better-Than-Expected Earnings and Lifts Its Outlook - Investopedia, accessed June 14, 2025, https://www.investopedia.com/adobe-earnings-q2-fy2025-11753218

Adobe just can't make investors happy, even after its strong earnings | Morningstar, accessed June 14, 2025, https://www.morningstar.com/news/marketwatch/20250613325/adobe-just-cant-make-investors-happy-even-after-its-strong-earnings

Adobe shares slump 7% as investors skeptical of quicker AI-adoption returns, accessed June 14, 2025, https://m.economictimes.com/markets/stocks/news/adobe-shares-slump-7-as-investors-skeptical-of-quicker-ai-adoption-returns/articleshow/121834255.cms

ADBE Q1FY25 Earnings Press Release - Adobe, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/21305202/a4t3greafe.pdf

Earnings call transcript: Adobe Q1 2025 beats earnings expectations - Investing.com, accessed June 14, 2025, https://www.investing.com/news/transcripts/earnings-call-transcript-adobe-q1-2025-beats-earnings-expectations-93CH-3925458

ADBE Q1FY25 Earnings Script and Slides - Adobe, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/21305202/c56hryhwgerfaw.pdf

Here's Where Traders Expect Adobe Stock To Go After Earnings - Investopedia, accessed June 14, 2025, https://www.investopedia.com/heres-where-traders-expect-adobe-stock-to-go-after-q2-2025-earnings-11752851

Adobe Posts Solid Q1 FY 2024 Quarter on $5.18B in Revenue - The Futurum Group, accessed June 14, 2025, https://futurumgroup.com/insights/adobe-posts-solid-q1-fy-2024-quarter-on-5-18b-in-revenue/

Here's Why Adobe Stock Declined by 26% in 2024 - Nasdaq, accessed June 14, 2025, https://www.nasdaq.com/articles/heres-why-adobe-stock-declined-26-2024

Adobe Reports Record Q4 and Fiscal 2024 Revenue, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/11214202/a56sthg53egr.pdf

Adobe Q4 FY2024 Earnings Call, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/11214202/c75e6yhrste.pdf

Adobe Reports Record Q4 and Fiscal 2024 Revenue, accessed June 14, 2025, https://www.adobe.com/content/dam/cc/in/about-adobe/newsroom/pdfs/2025/Adobe%20-%20Q4%20and%20FY24%20Earnings.pdf

Adobe Stock Falls: Time to Buy? | The Motley Fool, accessed June 14, 2025, https://www.fool.com/investing/2024/09/20/adobe-stock-falls-time-to-buy/

Adobe's Q3 2024 Earnings Show Continued Strength Across All Segments, accessed June 14, 2025, https://futurumgroup.com/insights/adobes-q3-2024-earnings-show-continued-strength-across-all-segments/

Adobe Reports Record Revenue in Q3 Fiscal 2024, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/au4736wy45tg.pdf

Adobe Inc. (ADBE), accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/pdf/corporate/investor-relations/q3-fy2024-earnings-transcript.pdf

What You Need To Know Ahead of Adobe's Earnings Report - Investopedia, accessed June 14, 2025, https://www.investopedia.com/what-you-need-to-know-ahead-of-adobe-earnings-report-thursday-8707135

Adobe Reports Record Revenue in Q1 Fiscal 2024, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/a4w5ergfj54.pdf

Adobe Reports Record Q4 and Fiscal 2023 Revenue, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/a56y5trgw.pdf

EDITED TRANSCRIPT - ADBE.OQ - Q4 2023 Adobe Inc Earnings Call EVENT DATE/TIME, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/pdf/corporate/investor-relations/q4-fy2023-earnings-transcript.pdf

Adobe Inc. (ADBE) Q4 2023 Earnings Call Transcript Summary - Moomoo, accessed June 14, 2025, https://www.moomoo.com/news/post/31067625/adobe-inc-adbe-q4-2023-earnings-call-transcript-summary

Adobe Revenue for Q3 2023 Again Sets a Record at $4.89 Billion - The Futurum Group, accessed June 14, 2025, https://futurumgroup.com/insights/adobe-revenue-for-q3-2023-again-sets-a-record-at-4-89-billion/

Adobe Reports Record Revenue in Q3 Fiscal 2023, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/aoiy4htrgf.pdf

EDITED TRANSCRIPT - ADBE.OQ - Q3 2023 Adobe Inc Earnings Call EVENT DATE/TIME, accessed June 14, 2025, https://www.adobe.com/cc-shared/assets/investor-relations/pdfs/q3-fy2023-earnings-transcript.pdf

Adobe (ADBE) Earnings Call Transcripts - Stocks - MLQ.ai, accessed June 14, 2025, https://mlq.ai/stocks/ADBE/earnings-call-transcripts/

Adobe (NASDAQ:ADBE) Reports Q3 In Line With Expectations - Barchart.com, accessed June 14, 2025, https://www.barchart.com/story/news/20281503/adobe-nasdaqadbe-reports-q3-in-line-with-expectations