Big Moves: December 20, 2024

What moved today and why? Novo Nordisk, Scholastic, Occidental Petroleum, Sirius XM, and more

Happy Holidays

This is our last note until 2025 as we tune out to tune into family. Priorities.

Before signing off, I’d like to share a few thoughts. First and foremost, thank you for reading. While I started Big Price Moves Explained as a largely self-indulgent exercise to reconnect with markets and get hands-on with AI, I also want to produce work that is valuable to others.

Ostensibly, that value is in explaining which stocks are moving on a given day and why. But for me, that’s just a small part of it. A newsletter is a blunt instrument—the reader has no control over the stocks covered. You get what you get. More universally, I hope, is the spark of imagination that comes from daily exposure to the magic of what AI can and cannot do.

Let’s start with what it can’t do. AI cannot create relevant and credible explanations without relevant and credible input. Some of you may be shouting at the screen right now that AI is, in fact, quite skilled at making things up—commonly referred to as “hallucinations”—but not for our purpose. With that in mind, I want to give a special shoutout to the folks at BigData.com and Tegus, in particular, for graciously providing the raw feedstock without which I’d have little to publish. Thank you.

Now, what AI can do is outright amazing. Folks who know me know that while I may be prone to repetition, I’m not one for hyperbole. But man, what I would have given to have access back in the day to what’s rolling out now... Wow. The ability to process overwhelming quantities of data, follow hand-wavey instructions, and deliver exactly what I want in the format I want is something to behold. The higher the value of your time, the higher the returns you can achieve. And the collective “we” is just getting started.

To wrap up, thank you again. As the AI era begins in earnest, I trust Big Moves is just getting going as well. Here’s to a 2025 we can hardly imagine—in the best possible way.

Editor’s Note: I am hitting send on Friday’s issue mid-day while the markets are still trading. The price changes below will be off a touch as a result.

For new readers, one of the main motivations behind starting Big Price Moves Explained was to have a reason to actively engage with AI on a daily basis—learning by doing. I maintain active editorial oversight over topic selection, model, and platform choices, but pretty much everything below this point is written by AI.

A quick preview of Friday’s notable moves (as of noon EST):

Mixed Results from Pharmaceuticals: Novo Nordisk* saw a significant drop after its experimental obesity drug fell short of expectations, while Dexcom’s stock rose, likely influenced by the performance of Eli Lilly, a competitor in the obesity treatment market.

Financial Struggles Impacting Stock Prices: Scholastic Corp.* faced a sharp decline following worse-than-expected quarterly results, highlighting how disappointing financials can weigh on a company’s stock.

The Visible Hand of Buffett: Occidental Petroleum and Sirius XM saw notable increases, with stock price boosts attributed to major investments by Berkshire Hathaway, signaling strong investor confidence in both companies.

* These companies have the pros and cons discussed on their earnings calls or in other materials summarized in the Read section below.

Skim

This is where you come to quickly see if anything interesting is happening with names you care about. Think of it as informative advertising.

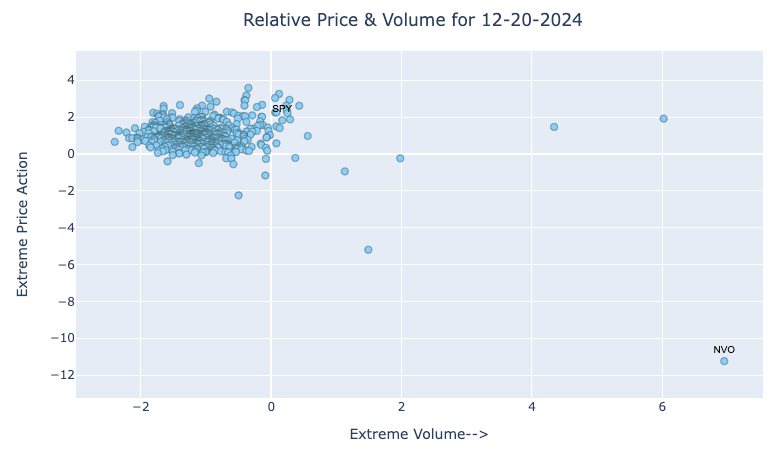

Novo Nordisk (NVO) - Pharmaceuticals (-20.3%) Novo Nordisk’s stock plummeted today after its experimental obesity drug, CagriSema, failed to meet weight-loss expectations in a late-stage trial. The trial results revealed that CagriSema achieved an average weight loss of 22.7%, falling short of the anticipated 25% and matching the efficacy of Eli Lilly’s competing drug, Zepbound. Sources: Reuters, MarketWatch, WSJ

Scholastic Corp. (SCHL) - Publishing (-14.81%) Scholastic’s stock is down 14.81% due to the company’s announcement of worse-than-expected Q2 financial results. The company reported earnings and revenue that lagged behind estimates, contributing to the decline in stock price. Sources: Investing.com via Web, Benzinga, Yahoo! Finance

Dexcom Inc (DXCM) - Medical Supplies (+7.32%) Dexcom’s stock increased by 7.32% due to its association with Eli Lilly, a rival obesity drug maker, whose shares jumped more than 4% following disappointing results from another company. This positive movement in Eli Lilly’s stock likely had a favorable impact on Dexcom, a maker of diabetes management devices. Sources: CNBC, Yahoo! Finance

Occidental Petroleum Corp. (OXY) - Oil & Gas Exploration & Production (+4.98%) Berkshire Hathaway, led by Warren Buffett, significantly increased its stake in Occidental Petroleum by acquiring approximately $409 million worth of shares, totaling around 8.9 million shares. Sources: Qrius, Zero Hedge, Benzinga, CNBC, MT Newswires, Investing.com via Web

Sirius XM Holdings Inc. (SIRI) - Broadcasting (+9.94%) Berkshire Hathaway’s purchase of approximately 4.96 million shares of Sirius XM Holdings at an average price of $21.60 led to a 9.94% increase in the stock price. Sources: CNBC, Benzinga, Investing.com via Web, Qrius

Powered by BigData.com, Big Price Moves Explained; text generated by GPT-4o

Read

In this section we offer a bit more detail in a couple of featured names.

Novo Nordisk (NVO) - Food Producers (-17.44%)

Phase 3 trial of CagriSema Disappoints

Novo Nordisk’s stock experienced its largest single-day decline in history, plummeting approximately 20% after disappointing trial results for its experimental weight loss drug CagriSema[1][9].

Trial Results

The Phase 3 trial of CagriSema, which lasted 68 weeks and involved about 3,400 participants, showed an average weight loss of 22.7%, falling short of the company’s anticipated 25% target[1][2]. The drug combines semaglutide, the active ingredient in Ozempic and Wegovy, with cagrilintide, which targets appetite suppression[3].

Key Findings:

Only 57% of participants reached the highest dosage level during the trial[2]

About 40.4% of participants achieved a weight loss of 25% or more[1]

The drug outperformed individual treatments of semaglutide (16.1%) and cagrilintide (11.8%)[2]

Market Impact

The disappointing results had significant implications for both Novo Nordisk and its competitors:

Stock Performance:

Novo Nordisk shares fell to their lowest level since August 2023[2]

Eli Lilly’s stock rose by approximately 5% following the news[3]

Other competitors like Viking Therapeutics saw their stock increase by 3%[1]

Competitive Landscape

The results have strengthened Eli Lilly’s position in the weight loss drug market. Their competing drug Zepbound achieved similar weight loss results of approximately 20% in clinical trials and is considered easier to manufacture[3]. Earlier this month, Eli Lilly’s Zepbound demonstrated superior results compared to Novo Nordisk’s Wegovy in a head-to-head trial, showing 20.2% weight loss versus 13.7% for Wegovy over 72 weeks[6].

Future Outlook

Despite the setback, Novo Nordisk plans to:

Continue development of CagriSema

Announce results from a second Phase 3 trial in early 2025[1]

Submit the drug for regulatory approval by the end of 2025[6]

The global market for weight loss medications is projected to reach $105 billion by 2030, driving intense competition among pharmaceutical companies[1].

Citations:

[1] https://qz.com/cagrisema-ozempic-drug-trial-1851726253

[2] https://www.investopedia.com/novo-nordisk-sinks-on-disappointing-trial-results-for-next-gen-weight-loss-drug-8764801

[3] https://markets.businessinsider.com/news/stocks/novo-nordisk-stock-price-weight-loss-drug-ozempic-eli-lilly-2024-1

[4] https://finance.yahoo.com/news/novo-nordisk-stock-declines-headline-162406408.html

[5] https://www.benzinga.com/government/regulations/24/12/42623343/exclusive-weight-loss-market-experts-scoop-up-novo-nordisk-stock-after-worst-drop-since-2002-following-drug-trial-miss

[6] https://www.nbcphiladelphia.com/news/business/money-report/novo-nordisk-shares-plunge-22-after-cagrisema-obesity-drug-trial-results/4059574/?os=qtfT_1%3Fno_journeys%3Dtrue

[7] https://finance.yahoo.com/video/eli-lilly-stock-pops-wegovy-165947113.html

[8] https://www.bloomberg.com/news/articles/2024-12-20/novo-next-generation-shot-helps-patients-lose-23-of-weight

[9] https://www.cnbc.com/2024/12/20/novo-nordisk-shares-plunge-22percent-after-cagrisema-obesity-drug-trial-results.html

[10] https://www.fastcompany.com/91250961/novo-nordisk-stock-price-falls-today-nvo-new-drug

Text written by Perplexity.ai

Scholastic Corp. (SCHL) - Publishing (-15.0%)

Bullish Thesis for Scholastic Challenged

The bullish thesis for Scholastic, which highlights the company's market leadership, financial strength, growth opportunities, and valuation upside, is challenged by its latest earnings report in several ways:

Revenue and Earnings Miss: Scholastic's second-quarter results for fiscal year 2025 were lower than the previous year, with revenues decreasing by 3% to $544.6 million. This is primarily due to the timing of their publishing schedule, particularly in the trade publishing division, with fewer major releases compared to the same period last year. Adjusted EBITDA for the second quarter was $108.7 million, down from $124 million a year ago. These results contradict the bullish expectation of strong and consistent financial performance. Additionally, Scholastic's second quarter earnings and revenue fell short of estimates.

Impact of Publishing Schedule: The timing of Scholastic’s publishing schedule, with fewer major releases in the second quarter of fiscal 2025, caused a decline in revenue compared to the previous year, when they recorded strong sales of multiple new titles. This indicates a vulnerability in the company’s reliance on a consistent stream of popular releases to drive sales. While new releases maintained a presence on bestseller lists, the overall revenue was still down.

Entertainment Segment Headwinds: While the acquisition of 9 Story Media Group was intended to expand Scholastic's entertainment capabilities, the segment is facing short-term challenges due to industry-wide budget cuts and production delays. This contradicts the bullish thesis that assumes smooth growth in this area. The segment's operating loss was $3.9 million due to increased amortization expenses and production expenses. These challenges have temporarily slowed, but not stopped, demand for production service work.

Education Solutions Segment Decline: The Education Solutions segment is experiencing a decline in sales due to reduced spending on supplemental curriculum products and lower revenues from state-sponsored programs. This contrasts with the bullish thesis of a strong presence in educational technology. Lower spending on supplemental curriculum products is a headwind for this business. The company expects to continue to face headwinds in this segment in fiscal 2025.

Book Fairs Revenue: Although School Book Fairs saw the largest number of fall fairs since the pandemic, overall revenue decreased slightly due to smaller fairs. The revenue per fair, while still high compared to pre-pandemic levels, has decreased slightly. This suggests that the company's growth in the number of fairs is not fully translating into proportional revenue growth.

Free Cash Flow: The free cash flow was $42.4 million in the second quarter, compared to $88.6 million in the prior-year period, primarily reflecting lower operating cash flow. While the bullish thesis mentions a free cash flow of $60 million in the latest fiscal year, the recent quarterly results demonstrate some variability. The company anticipates a full-year free cash flow of between $20 and $30 million.

Analyst Price Target: While an analyst price target of $54 suggests significant upside, the recent earnings miss may cause analysts to reevaluate. The current intrinsic value is estimated at $49.09 vs a market price around $22, but the market may take time to recognize the company's true value in light of earnings misses.

Debt: The company had borrowings of $250 million under its revolving credit facility. Net debt was $120.8 million at the end of the quarter, compared to a net cash position of $107.7 million at the end of fiscal year 2024. This indicates that the company has taken on debt to finance operations and acquisitions, which challenges the bullish point that Scholastic maintains minimal debt. While the company is comfortable with its leverage, it indicates an increase in debt.

Despite these challenges, Scholastic has reaffirmed its fiscal year 2025 guidance, expecting revenue growth of 4% to 6% and adjusted EBITDA of $140 million to $150 million. The company is actively adapting to market changes and investing in long-term growth, but the earnings report highlights the vulnerabilities and challenges to the bullish thesis, which are important for investors to understand.

Source: BigData.com, Factset, Big Price Moves Explained; text generated by Google’s NotebookLM

Disclaimer: The information contained in this newsletter is intended for educational purposes only and should not be construed as financial advice. Please consult with a qualified financial advisor before making any investment decisions. Additionally, please note that we at e/r/c advisors may or may not have a position in any of the companies mentioned herein. This is not a recommendation to buy or sell any security. The information contained herein is presented in good faith on a best efforts basis; note that most of the writing is undertaken by AI—rely on it at your own risk.