Big Moves: June 20, 2025

What moved today and why? Kroger, Accenture and Cognizant

The Three Witches

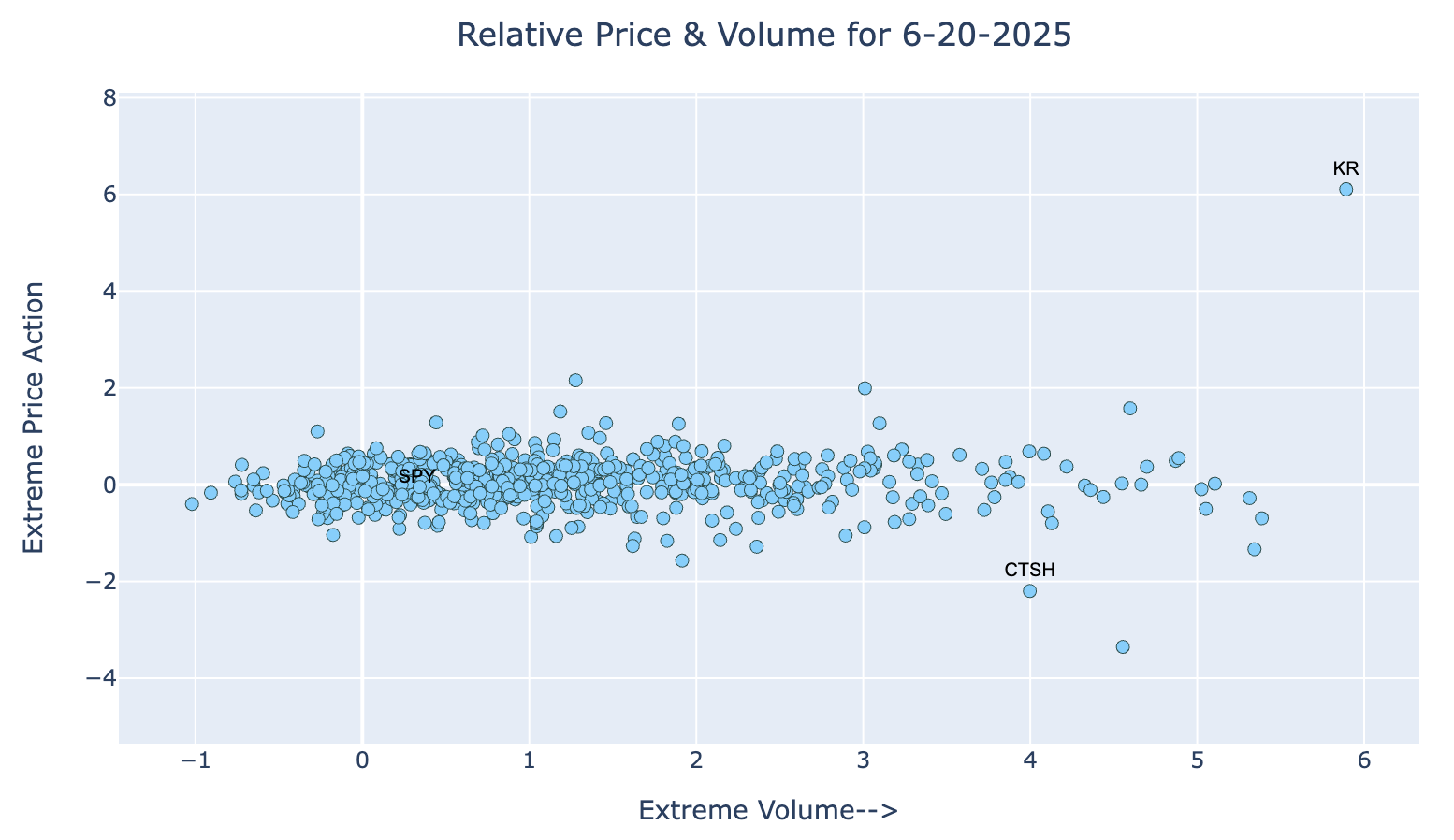

The scatter plot below should look odd to longtime readers of Big Moves. Normally, there’s a big blob of dots squished on the left, with a few outliers in the upper left and right corners. For newbies, the up-and-down axis captures the relative size of price moves, while the left-right axis measures volume. You can often see large price changes on normal volume, but it’s rare to see extraordinary volume without a commensurate move in price.

There are two notable exceptions to the above rule of thumb: major index rebalances and Triple Witching. These are well-known and highly advertised events, with mostly balanced supply-demand dynamics. During my hedge fund days, we spent a lot of effort understanding the ins and outs of the likely impacts. These impacts matter when one is trading with borrowed money, but for most folks, the swings on these days should be ignored—or, at most, treated as opportunities to fade the noise.

Friday was a 3W day. Triple Witching refers to the simultaneous expiration of three distinct types of derivative contracts on the same trading day. For those looking to dig a bit deeper, I’ve pulled together a primer here.

For new readers, one of the main motivations behind starting Big Price Moves Explained was to have a reason to actively engage with AI on a daily basis—learning by doing. I maintain active editorial oversight over topic selection, model, and platform choices, but pretty much everything below this point is written by AI.

A quick preview of Friday’s notable moves:

Outlook Sensitivity: Stocks rallied or tumbled based largely on future-facing guidance, not current performance—evident in both Kroger’s* gains and Accenture’s* drop.

Cost Aversion: Market punished large-scale spending, as seen with Cognizant's decline despite a jobs-creating expansion, suggesting caution around long-term capital outlays.

Expectations Gap: Modest disappointments in forecasts, even with solid fundamentals, were enough to drag down major names, underlining the tightrope companies walk with investor expectations.

* These companies have the pros and cons discussed on their earnings calls or in other materials summarized in the Read section below.

Skim

This is where you come to quickly see if anything interesting is happening with names you care about. Think of it as informative advertising.

Kroger Co. (KR) - Food & Drug Retailers (71.97 | +9.84%) Kroger Co. (KR) shares increased by 9.84% on June 20, 2025, primarily due to the company raising its full-year identical sales growth outlook. The company reported first-quarter results that exceeded earnings estimates, with adjusted EPS of $1.49 compared to the expected $1.46, and announced a new identical sales growth forecast of 2.25% to 3.25%, up from the previous 2% to 3% range, which was positively received by the market. Sources: Washington Post, CNBC, The Fly, Benzinga, MT Newswires

Accenture plc (ACN) - Support Services (285.37 | -6.86%) Accenture plc (ACN) is down -6.86% due to a decline in quarterly new bookings and a reduction in its revenue guidance. The company reported a 6% drop in bookings to $19.70 billion, which was below expectations and followed a previous decline, indicating ongoing challenges in securing future revenue. Additionally, Accenture’s revised revenue growth guidance of 6% to 7% for the fiscal year, with a constant-currency revenue guidance of 1%-5%, was seen as modestly disappointing, suggesting a lower starting point for FY26 compared to Street estimates. Sources: BNN Bloomberg, Edgar SEC Filings, The Fly, Benzinga, MT Newswires

Cognizant Technology Solutions Corp. (CTSH) - Computer Services (75.47 | -4.64%) Cognizant Technology Solutions Corp. (CTSH) is down -4.64% on the day following the announcement of its substantial investment in a new IT campus in Visakhapatnam, India. The company plans to invest INR1,582.98 crore to establish the campus, which will create approximately 8,000 jobs by 2029. Despite the positive long-term outlook, the market may be reacting to the immediate financial implications of such a significant investment, especially in a climate where global IT companies are taking cost-cutting measures due to demand uncertainty. Sources: The Times Of India, The Hindu via Web, BusinessLine via Web, Business Standard via Web

Powered by BigData.com, Big Price Moves Explained; text generated by GPT-4o

Read

In this section we offer a bit more detail in a couple of featured names.

Accenture plc (ACN) - Support Services (285.37 | -6.86%)

Deep Dive on Accenture Lifts Outlook on Strong Q3 Results, but Bookings Slump Weighs on Shares Earnings

Accenture (NYSE: ACN) reported strong third-quarter fiscal 2025 results with revenues of $17.73 billion (8% growth) and EPS of $3.49 (15% increase), yet experienced a 5–11% stock decline primarily due to disappointing bookings performance, marking the second consecutive quarter where robust financial metrics were overshadowed by concerns about future revenue pipeline and federal government spending cuts.

Financial Performance Highlights

The third quarter saw Accenture's operating margin improve to 16.8%, an 80 basis point increase year-over-year, contributing to a 13% rise in GAAP operating income to $2.98 billion. Revenue growth was broad-based across segments, with Consulting growing 7% to $9.01 billion and Managed Services increasing 9% to $8.72 billion. Geographically, the Americas led with 8% growth to $8.97 billion, while EMEA grew 8% to $6.23 billion, and Asia Pacific increased 5% to $2.53 billion.

Free cash flow remained robust at $3.5 billion, enabling the company to return $2.7 billion to shareholders through repurchases and dividends, including a quarterly cash dividend of $1.48 per share (15% increase over the previous year). Based on these strong results, Accenture raised its full-year guidance, now projecting 6–7% revenue growth in local currency (up from 5–7%), operating margin of 15.6%, and diluted EPS of $12.77–$12.89, representing a 12–13% increase over fiscal 2024.

Bookings Decline Concerns

New bookings for the quarter totaled $19.7 billion, representing a 6% decrease in U.S. dollars and 7% in local currency compared to the same period last year, falling short of analyst expectations of $20.03 billion. This marked the second consecutive quarter of declining bookings, raising investor concerns about Accenture's near-term outlook despite strong financial performance. JPMorgan analysts specifically highlighted that "forward-looking metrics such as bookings (and headcount this quarter) came in weaker than expected," while Jefferies noted that the updated guidance "implies growth will continue to slow down and the growth issue is further reinforced by the decline in bookings."

Despite this overall decline, Accenture reported substantial growth in generative AI new bookings, which reached $1.5 billion for the quarter and approximately $7.1 billion since the company began reporting these figures separately. The company also highlighted its success in securing 30 clients with quarterly bookings exceeding $100 million, demonstrating the strength of its key client relationships despite the broader bookings challenges.

Federal Spending Impact

The federal services unit, representing approximately 8% of Accenture's global revenue and 16% of Americas revenue in fiscal 2024, faced significant pressure from the Trump administration's efficiency initiatives. CEO Julie Sweet explicitly acknowledged that "many new procurement actions have slowed, which is negatively impacting our sales and revenue," as the administration pursued its "clear goal to run the federal government more efficiently."

This headwind persisted throughout 2025, with the General Services Administration's directive to review and cancel non-essential consulting contracts creating ongoing challenges. The Department of Government Efficiency, led by Elon Musk, continued to implement federal spending cuts that weighed heavily on Accenture's government business segment, contributing to investor concerns despite the company's strong performance in other sectors.

Strategic Reorganization

In a significant strategic shift announced alongside its Q3 earnings, Accenture will consolidate all of its services—Strategy, Consulting, Song, Technology, and Operations—into a single integrated business unit called "Reinvention Services" effective September 1, 2025. This represents the most substantial structural change in the company's recent history and will be led by Manish Sharma, current CEO of the Americas, who will become Accenture's first Chief Services Officer. The reorganization aims to "create more leading solutions faster and embed data and AI more easily" into solutions and delivery, according to CEO Julie Sweet, who emphasized this transformation will make it "even easier to bring those solutions, embed data and AI, so we can really scale across our client base and into new markets." JPMorgan analysts noted that these "leadership changes naturally raises questions," contributing to investor uncertainty despite the improved financial outlook.

Then and Now

Guided by Big Price Moves Explained; Sourced and written with Perplexity.ai in Deep Research mode [link with citations]

Kroger Co. (KR) - Food & Drug Retailers (71.97 | +9.84%)

Kroger Stock Surges After Retailer Lifts Guidance on Robust Identical-Store Sales Growth

Kroger Co. (KR) shares surged 9.84% on June 20, 2025, after the grocery giant reported first-quarter earnings that exceeded analyst expectations with adjusted EPS of $1.49 versus the anticipated $1.46, while also raising its full-year identical sales growth forecast to 2.25%-3.25% from the previous 2%-3% range.

Financial Performance Highlights

The first quarter of 2025 showcased Kroger's operational strength with identical sales without fuel increasing 3.2% compared to just 0.5% in the prior year period, significantly outpacing analyst expectations of 2.4% growth. Total revenue reached $45.12 billion, slightly missing the consensus estimate of $45.19 billion. Gross margin improved significantly to 23.0% from 22.0% in the prior year, primarily due to the sale of Kroger Specialty Pharmacy, lower shrink, and reduced supply chain costs.

Operating profit grew to $1,322 million from $1,294 million year-over-year, while adjusted FIFO operating profit reached $1,518 million. The company's e-commerce segment showed particularly strong performance with 15% growth, supported by improvements in order accuracy and reduced pickup wait times. Despite these positive results, Kroger recognized a $100 million impairment charge related to planned closures of approximately 60 stores over the next 18 months.

Management Commentary

Interim Chairman and CEO Ron Sargent highlighted the company's strong performance, stating, "Kroger delivered solid first quarter results, with strong sales led by pharmacy, eCommerce and fresh." Sargent emphasized the company's progress in "streamlining our priorities, enhancing customer focus, and running great stores to improve the shopping experience" while expressing confidence in Kroger's strategic direction and ability to "build on our momentum, deliver value for customers, invest in associates and generate attractive returns for shareholders."

CFO David Kennerley, who joined from PepsiCo in April 2025, offered measured optimism about the raised guidance while acknowledging economic uncertainties. "Our strong sales results and positive momentum give us confidence to raise our identical sales without fuel guidance," Kennerley noted, while cautioning that "the macroeconomic environment remains uncertain and as a result other elements of our guidance remain unchanged." This balanced outlook reflects the leadership team's strategic approach during the ongoing executive transition following former CEO Rodney McMullen's resignation in March 2025.

Market Response

Wall Street reacted enthusiastically to Kroger's earnings report, making the stock the top performer in the S&P 500 on June 20, 2025, with a surge that significantly exceeded the ±4.7% move options traders had anticipated. This performance was particularly impressive considering Kroger historically averages only a +3.3% return on earnings days. The broader market context made Kroger's gains even more notable, as the S&P 500 slid 0.2% that day amid investor concerns about ongoing conflicts in the Middle East.

Analyst sentiment remains predominantly positive, with 15 analysts maintaining a consensus "Buy" rating and an average price target of $69.47. The analyst community shows strong confidence with 72.46% BUY ratings versus only 1.45% SELL ratings. Recent analyst actions include Morgan Stanley raising their price objective to $71.00 while maintaining an "equal weight" rating, though Melius Research had previously downgraded Kroger to "Sell" with a $58 price target, citing competitive pressure from Walmart's growing market share.

Strategic Initiatives

Amid competitive pressures in the grocery retail sector, Kroger is implementing several strategic initiatives to maintain its market position. The company plans to close approximately 60 underperforming stores over the next 18 months, with management expecting modest financial benefits that will be reinvested into customer experience improvements. Kroger's "Our Brands" private label portfolio continues to outperform national brands for the seventh consecutive quarter, with 80 new protein items launched under this line in Q1 2025.

The company has centralized its e-commerce operations under Chief Digital Officer Yael Cosset to enhance focus and accountability, supporting the 15% growth in this segment. With a net total debt to adjusted EBITDA ratio of 1.69, Kroger maintains financial flexibility for its planned capital expenditures of $3.6-$3.8 billion in fiscal 2025, which will fund store renovations, digital capabilities, and supply chain enhancements while supporting its reputation as a dividend growth stock with 19 consecutive years of increases.

Guided by Big Price Moves Explained; Sourced and written with Perplexity.ai in Deep Research mode [link with citations]

Disclaimer: The information contained in this newsletter is intended for educational purposes only and should not be construed as financial advice. Please consult with a qualified financial advisor before making any investment decisions. Additionally, please note that we at e/r/c advisors may or may not have a position in any of the companies mentioned herein. This is not a recommendation to buy or sell any security. The information contained herein is presented in good faith on a best efforts basis; note that most of the writing is undertaken by AI—rely on it at your own risk.