Big Moves: June 13, 2025

What moved today and why? Visa, Mastercard, Adobe, Oracle and more

Confidence Not Shared

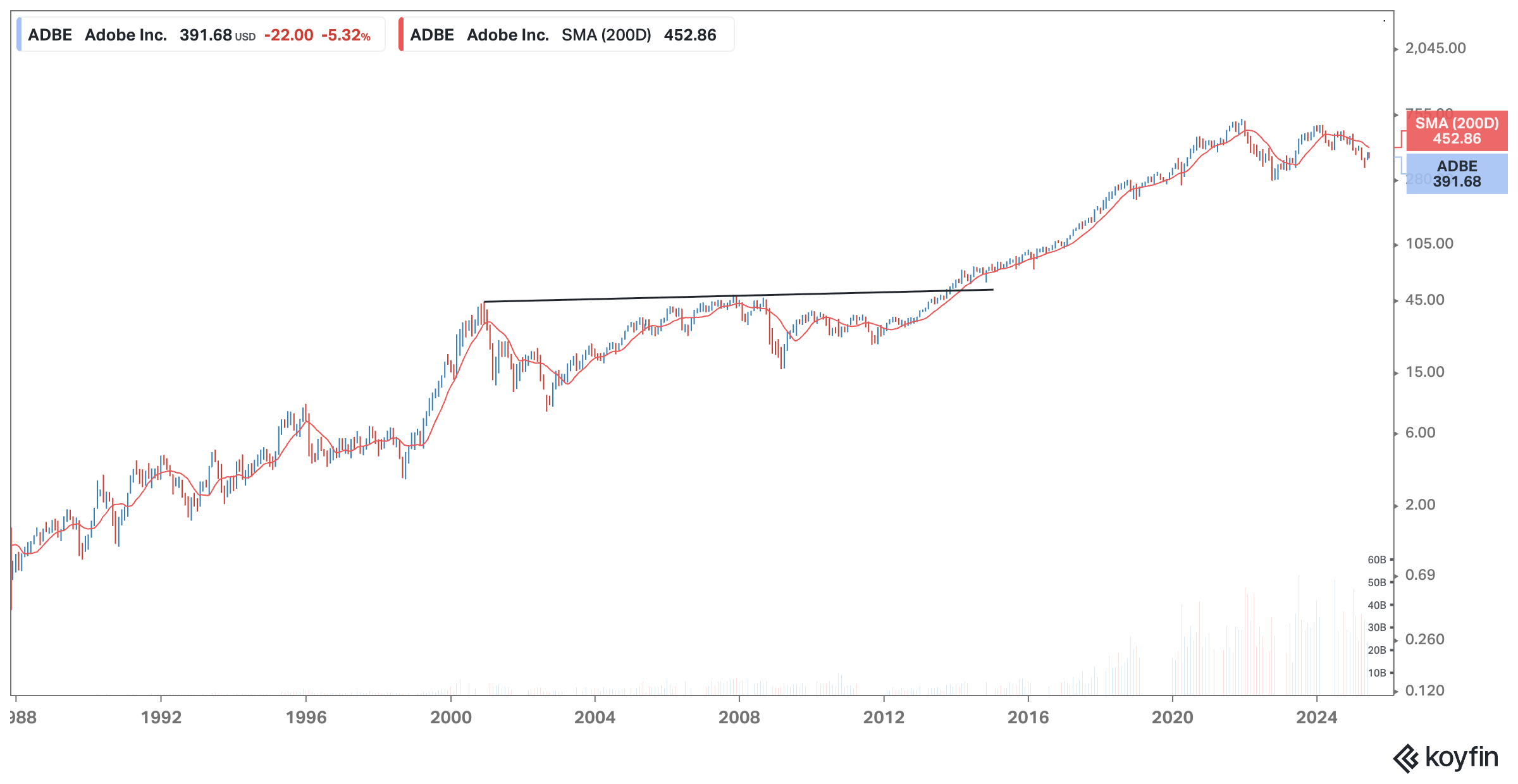

This is not the first time Adobe has led off one of these notes. Friday marked the seventh out of the last eight earnings reports where the stock sold off more than four percent on the day. Indeed, down five percent feels like good news. Perhaps the most baffling part is that the company has delivered better-than-expected results every time. Not a miss.

What is missing? In a word: confidence—or the lack thereof. At the heart of investors’ concerns is the pace at which Adobe is, or isn’t, converting its considerable AI investments into revenue and profits. Colloquially, this is referred to as monetization.

I asked Google’s Gemini model to research on our behalf whether there has been a common concern threaded through the past eight quarters of disappointment. I encourage you to read its full report here: Adobe's Persistent Post-Earnings Sell-Offs: Identifying the Common Themes. The short answer is that the market is afraid Adobe won’t get its money back.

For new readers, one of the main motivations behind starting Big Price Moves Explained was to have a reason to actively engage with AI on a daily basis—learning by doing. I maintain active editorial oversight over topic selection, model, and platform choices, but pretty much everything below this point is written by AI.

A quick preview of Friday’s notable moves:

Investor Skepticism: Shares of Adobe* fell sharply despite strong earnings and upbeat guidance, as doubts over the monetization timeline for its AI initiatives dominated sentiment.

Strong Outlook: Oracle surged after not only topping earnings expectations but also issuing guidance well above forecasts, with analysts rushing to raise their targets.

Disruption Risk: Both Visa* and Mastercard were hit hard by reports that major retailers are exploring stablecoin alternatives, raising alarms over future fee-based revenue.

Valuation Pressure: PG&E dropped following a price target cut tied to persistent regulatory concerns and past wildfire liabilities.

* These companies have the pros and cons discussed on their earnings calls or in other materials summarized in the Read section below.

Skim

This is where you come to quickly see if anything interesting is happening with names you care about. Think of it as informative advertising.

Oracle Corp. (ORCL) - Software (+7.69%) Oracle Corp. (ORCL) is up 7.69% following the previous day’s 13% jump, primarily due to the strong momentum in its cloud business as highlighted in its recent earnings report. The company's revenue and earnings exceeded estimates, and CEO Safra Catz provided revenue guidance for the next fiscal year that was significantly above consensus, indicating robust future growth prospects. Additionally, multiple analysts have upgraded their price targets for Oracle, further contributing to the stock's rally. Sources: Forbes.com via Web, CNBC, Alliance News, Benzinga

Adobe Inc. (ADBE) - Software (-5.32%) Adobe Inc. (ADBE) shares fell 5.32% on June 13, 2025, primarily due to investor skepticism about the company's timeline for realizing returns from its AI integration. Despite Adobe reporting better-than-expected second-quarter financial results and raising its full-year 2025 revenue and earnings guidance, concerns over the pace of AI adoption overshadowed these positive developments. Additionally, at least five brokerages cut their price targets for Adobe following the earnings announcement, contributing to the stock's decline. Sources: BNN Bloomberg, Benzinga, The Fly

Visa Inc (V) - Consumer Finance (-4.99%) Visa Inc (V) is down 4.99% primarily due to reports that major retailers are exploring the use of stablecoins to bypass traditional credit card payment fees. This development, reported by The Wall Street Journal, suggests that large multinational merchants, including Walmart and Amazon, may issue their own stablecoins, potentially reducing reliance on Visa's payment network. This news has raised concerns about future revenue streams from transaction fees, leading to a significant drop in Visa's stock price. Sources: Yahoo! Finance, Nasdaq, MT Newswires, The Fly

Mastercard Incorporated (MA) - Consumer Finance (-4.62%) Mastercard Incorporated (MA) is down 4.62% due to a Wall Street Journal report indicating that major retailers like Walmart and Amazon are considering launching their own stablecoins. This development poses a potential threat to traditional payment processors like Mastercard, as stablecoins could bypass existing payment networks and reduce card processing fees. Sources: Yahoo! Finance, MT Newswires, Benzinga, The Fly

PG&E Corp. (PCG) - Conventional Electricity (-4.62%) Jefferies cut its price target on PG&E Corp. (PCG) stock to 19from22, which is the most likely reason for the stock's decline of 4.62% on June 13, 2025. This adjustment reflects a reassessment of the company's valuation, possibly due to ongoing regulatory challenges and its history with wildfire incidents. Sources: Yahoo! Finance, MT Newswires, Seeking Alpha

Powered by BigData.com, Big Price Moves Explained; text generated by GPT-4o

Read

In this section we offer a bit more detail in a couple of featured names.

Adobe Inc. (ADBE) - Software (391.68 | -5.32%)

Thirteen-plus years in the desert… Let’s hope past is not prolog.

Adobe Lifts Outlook, But Wall Street Seeks Clearer AI Monetization Path

Adobe shares fell 7% in early trading on June 13, 2025, as investor skepticism about the timeline for realizing returns from AI integration overshadowed the company's better-than-expected Q2 financial results and raised full-year guidance.

Financial Performance Highlights

Record revenue of $5.87 billion was achieved in Q2 fiscal year 2025, representing an 11% year-over-year growth that exceeded Wall Street projections of $5.79 billion. The company reported impressive earnings with GAAP diluted EPS of $3.94 and non-GAAP EPS of $5.06, surpassing analyst estimates of $4.96–$4.97 per share and showing 13% year-over-year growth.

The Digital Media segment contributed $4.35 billion with 11% year-over-year growth, while its annualized recurring revenue (ARR) reached $18.09 billion, growing 12.1% year-over-year. Digital Experience segment generated $1.46 billion, up 10% from the previous year, with subscription revenue within this segment rising 11% to $1.33 billion. Operating cash flow hit $2.19 billion, and the company maintained strong remaining performance obligations (RPO) of $19.69 billion, with 67% classified as current.

Management Commentary and Strategy

During the earnings call, CEO Shantanu Narayen emphasized Adobe's position at the forefront of AI-driven creative economy transformation, stating that "Adobe's AI innovation is transforming industries enabling individuals and enterprises to achieve unprecedented levels of creativity." The company reported significant momentum in AI adoption metrics, with over 24 billion cumulative AI generations across Creative Cloud and Firefly applications, while monthly active users for the combined Acrobat and Express platforms exceeded 700 million, growing over 25% year-over-year.

CFO Dan Durn reinforced management's confidence in the company's AI trajectory, noting: "As a result of us driving strong performance in the first half of the year, we are pleased to raise Adobe's FY25 total revenue and EPS targets. We continue to invest in AI innovation across our customer groups to enhance value realization and expand the universe of customers we serve." For Q3 2025, Adobe projects revenue of $5.88–$5.93 billion and adjusted EPS of $5.15–$5.20, above consensus projections.

Analyst Reactions and Concerns

At least five brokerages reduced their price targets for Adobe following the earnings announcement, contributing significantly to the stock's decline. Wells Fargo analyst Michael Turrin maintained an Overweight rating while raising his price target from $430 to $470, whereas Oppenheimer's Brian Schwartz lowered his target from $530 to $500 while maintaining an Outperform rating. BMO Capital's Keith Bachman and Evercore ISI's Kirk Materne both maintained Outperform ratings with price targets of $450 and $475 respectively.

CFRA Research analyst Angelo Zino expressed particular concern about "growing worries about competitive challenges and an extended timeline to achieve significant monetization from AI," reducing his price target from $575 to $500. RBC analysts captured the prevailing sentiment, noting that "although the guidance has been improved and management is optimistic about demand generation, it appears that more time will be required to validate these AI initiatives and alleviate concerns regarding competition in the generative AI space."

AI Monetization Timeline Challenges

Despite raising its fiscal 2025 revenue projection to between $23.50 billion and $23.60 billion (up from previous estimates), Adobe faces significant investor skepticism regarding its AI monetization timeline. The company's AI-influenced annual recurring revenue (ARR) is already contributing billions of dollars, with a target to exceed $250 million by the end of fiscal 2025, but this represents only a small fraction of Adobe's overall revenue. Wall Street analysts have highlighted Adobe's struggle to articulate a clear path toward monetizing its AI technologies, with Bernstein analyst Mark Moerdler noting the difficulty investors have in reconciling Adobe's optimistic AI outlook with its current performance metrics.

The market's reaction reflects broader concerns about the return on investment timeline for Adobe's substantial AI expenditures. While Adobe's Firefly and Creative Cloud tools have seen rapid adoption with over 24 billion generations by the end of Q2, the company faces intensifying competition from both established players and nimble startups in the generative AI space. This competitive landscape, combined with Adobe's delayed entry compared to companies like Stability AI and Midjourney, has contributed to investor uncertainty about whether Adobe can maintain its leadership position in creative software as AI capabilities become increasingly commoditized. The upcoming Adobe Summit is viewed as a critical opportunity for the company to demonstrate a more concrete monetization model for its AI investments and potentially restore investor confidence.

Guided by Big Price Moves Explained; Sourced and written with Perplexity.ai in Deep Research mode [link with citations]

Visa Inc (V) - Consumer Finance (352.85 | -4.99%)

Visa, Mastercard Lose $60 Billion in Market Value Amid Stablecoin Disruption Fears

Visa Inc. shares fell nearly 5% on June 13, 2025, after The Wall Street Journal reported that major retailers including Walmart and Amazon are exploring issuing their own stablecoins, potentially bypassing traditional payment networks and threatening the billions in transaction fees collected by credit card companies.

Stablecoin Threat from Retailers

The retail giants' exploration of stablecoins represents a direct challenge to traditional payment processors, with Amazon, Walmart, Expedia Group, and several major airlines discussing the launch of corporate stablecoins. These blockchain-based payment systems would allow merchants to significantly reduce transaction costs, speed up settlement times, and enhance global e-commerce operations. The Wall Street Journal's report triggered widespread selling pressure across the payments sector, with Mastercard dropping 4.6%, American Express declining 2%, and the combined market capitalization loss for Visa and Mastercard exceeding $60 billion in a single trading session.

Stablecoins maintain a one-to-one exchange ratio with government currencies and are backed by cash reserves or Treasury securities, offering a potentially more cost-effective alternative to traditional card processing. The stablecoin market has grown substantially, with monthly transaction volumes exceeding $710 billion as of March 2025, approaching Visa's $1 trillion monthly processing volume. In 2024, stablecoins facilitated more than $27.6 trillion in transactions, surpassing the combined volumes of Visa and Mastercard.

Financial Impact on Visa

The potential adoption of stablecoins by major retailers threatens Visa's substantial revenue streams from transaction processing. With $37.62 billion in trailing twelve-month revenue as of March 2025 (a 10.19% year-over-year increase), Visa's business model heavily depends on data processing fees ($4.7 billion), service fees ($4.4 billion), and international transaction fees ($3.3 billion) from its most recent quarter.

The scale of possible disruption becomes evident when considering that credit and debit card "swipe fees" totaled $224 billion in 2023, with Visa and Mastercard credit card processing fees alone exceeding $100 billion. These fees typically range from 2–4% of each transaction and represent merchants' highest operating cost after labor. If retail giants like Amazon (with $638 billion in annual revenue) and Walmart (with global e-commerce sales surpassing $100 billion) successfully implement stablecoin payment systems, billions in transaction volume could be diverted away from traditional payment networks.

Regulatory Framework

The retailers' stablecoin initiatives hinge on the passage of the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act of 2025, which would create a comprehensive regulatory framework for stablecoin issuance in the United States. After clearing a crucial procedural vote 68–30 on June 11, the bill is scheduled for a final Senate vote on June 17, 2025, before proceeding to the House of Representatives where a separate version is under consideration.

President Donald Trump has prioritized cryptocurrency clarity, pushing for stablecoin legislation by August 2025, with his administration's pro-stablecoin stance accelerating corporate adoption. The market is already seeing movement, with Ripple launching RLUSD last year, while Wall Street clearinghouse DTCC and major banks have reportedly discussed fiat-backed stablecoin launches. Platforms like Shopify have partnered with Coinbase and Stripe to integrate Circle's USDC, while market leader Tether plans to issue a U.S.-specific stablecoin targeting domestic institutional investors.

Industry Response

Despite the immediate stock decline, several Wall Street analysts view this as a buying opportunity rather than a reason for panic. Analysts from William Blair specifically advised investors to take advantage of the price dip, maintaining positive outlooks on both Visa and Mastercard despite the potential long-term threat from stablecoin adoption.

The payment industry is already responding to this challenge, with major U.S. banks including JPMorgan, Bank of America, Citigroup, and Wells Fargo reportedly considering issuing a joint stablecoin to compete with digital asset platforms. Technology companies are also exploring stablecoin integration, with Apple, Airbnb, Google, and Elon Musk's X platform reportedly in early discussions with cryptocurrency companies about incorporating stablecoins into their payment systems to reduce transaction costs and streamline international payments.

Guided by Big Price Moves Explained; Sourced and written with Perplexity.ai in Deep Research mode [link with citations]

Disclaimer: The information contained in this newsletter is intended for educational purposes only and should not be construed as financial advice. Please consult with a qualified financial advisor before making any investment decisions. Additionally, please note that we at e/r/c advisors may or may not have a position in any of the companies mentioned herein. This is not a recommendation to buy or sell any security. The information contained herein is presented in good faith on a best efforts basis; note that most of the writing is undertaken by AI—rely on it at your own risk.